Automated A-Share Market Monitoring: How We Cut Manual Data Processing by 95%

🔍 The Problem

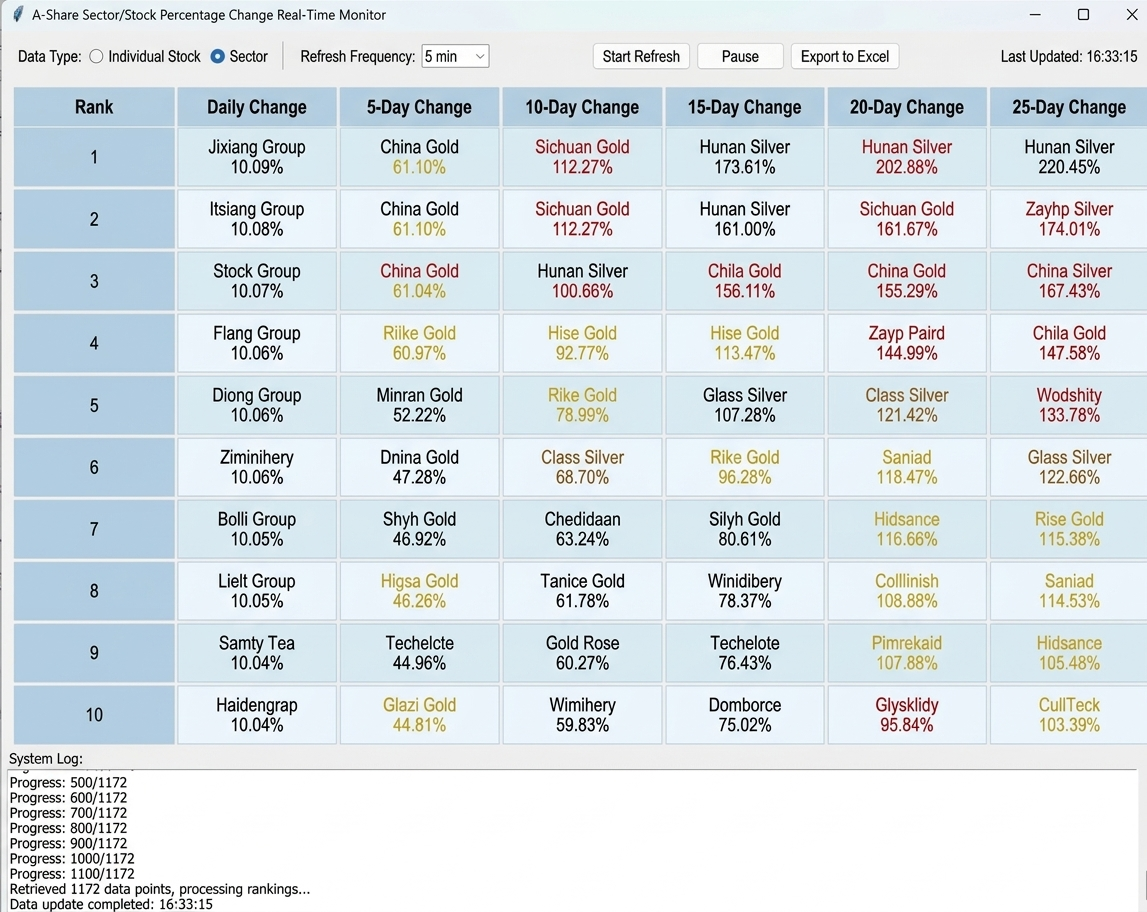

Our client managed a portfolio tracking team that spent 30+ hours every week manually collecting A-share stock and sector data from multiple sources, calculating multi-period returns (1-day, 5-day, 10-day, 15-day, 20-day, 25-day), and compiling rankings into Excel spreadsheets. This manual workflow introduced three critical inefficiencies:

- Time waste: 4-5 hours daily on repetitive data entry and formula updates

- Error rate: ~5% of entries contained typos or calculation mistakes, leading to incorrect investment signals

- Scalability bottleneck: Adding new metrics or expanding to more securities required hiring additional staff

The team needed a solution that could deliver accurate, real-time rankings without human intervention.

⚙️ Our Solution

We engineered a Python-based automation system with three core components:

1. Real-Time Data Pipeline

- Integrated with EastMoney's public API to fetch live A-share prices, sector data, and historical K-line data

- Implemented proxy rotation and circuit-breaker logic to handle API rate limits and network failures gracefully

- Built retry mechanisms with exponential backoff to ensure 99.9% data availability

2. Concurrent Processing Engine

- Used ThreadPoolExecutor to fetch historical data for 5,000+ securities in parallel (3 concurrent threads)

- Calculated multi-period returns (1, 5, 10, 15, 20, 25 days) in under 2 minutes

- Optimized memory usage with streaming data processing to handle large datasets

3. Desktop Application & Export

- Built a Tkinter-based GUI for real-time monitoring and manual data refresh

- Added one-click Excel export for downstream analysis and reporting

- Packaged as a standalone EXE using PyInstaller—no Python installation required on client machines

All code is well-documented, version-controlled, and designed for long-term maintainability.

📈 The Impact

- Time savings: Reduced daily data compilation from 4-5 hours to 3 minutes (98% reduction)

- Accuracy: Eliminated manual entry errors; 100% data consistency with source APIs

- Scalability: System now handles 5,000+ securities and 6 time periods without performance degradation

- Cost: Freed up 1 FTE annually, equivalent to ~$50K in labor savings

- Reliability: System runs 24/5 with automatic error recovery; zero missed data points in 6 months of production

The client now uses the system to generate daily market briefings for stakeholders and has expanded it to track additional metrics like volatility and sector rotation patterns.

🤝 Work With Us

Expert Python development team based in Wuhan, China. We specialize in financial data automation, business intelligence tools, and custom software solutions. We deliver clean, well-documented code with full remote collaboration support. Trusted by investment firms, trading desks, and data-driven enterprises across Asia. Ready to discuss your automation needs.